Mobile payment mainly refers to the transfer of monetary value through mobile communication devices and the use of wireless communication technology to clear the creditor-debtor relationship. The basis of mobile payment is the popularity of mobile terminals and the development of mobile Internet. Mobility is its biggest feature. With the increase of mobile terminal penetration rate, in the future, mobile payment is completely possible to replace cash and bank cards, which is generally accepted by people in commodity labor transactions and debts and debts, and becomes a major form of electronic money. 5.70mm Wire To Board Connectors 5.70mm Wire to Board,Wire To Board Connectors 5.70mm Wire to Board,Wire To Board Connectors ShenZhen Antenk Electronics Co,Ltd , https://www.antenksocket.com

According to statistics, in 2013, the global mobile payment scale reached 1.45 trillion yuan, a year-on-year increase of 45%; and the average annual growth rate from 2009 to 2013 exceeded 60%. In 2013, the number of mobile payment users worldwide exceeded 245 million, an increase of 22% over the same period of last year. In 2012, the domestic mobile payment market was 151.1 billion yuan. In 2013, the market scale exceeded 300 billion yuan, an increase of 89% over the same period of last year. The transaction volume of mobile payment market grew rapidly, and the transaction scale mainly came from the remote payment service based on mobile internet. .

By the end of 2013, Alipay's real-name users had reached 300 million. In the past year, Alipay completed 12.5 billion payments, while Alipay's wallet users exceeded 100 million. In 2013, more than 2.78 billion and more than 900 billion were paid through Alipay mobile payment. Yuan's payment, in this calculation, Alipay has become the world's largest mobile payment company.

First, the principle of mobile payment

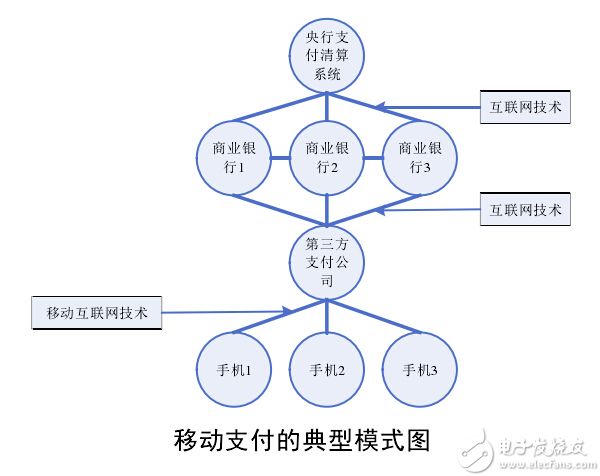

A typical mobile payment model generally requires the cooperation of third party payment, such as WeChat payment and Alipay payment (as shown). The generation of third-party payment makes the customer not directly pay with the bank for payment and settlement. The advantages are as follows: First, it can play a guarantee role in e-commerce. Second, third-party payment can be integrated into many banks, and payment can be made without opening online banking and mobile banking. Third, it can save transaction costs. Mobile payment is on the surface of transferring payment terminals from the computer to the mobile phone, etc., but this transfer may lead to revolutionary changes in the payment field, because payment is the transfer of money between different accounts, and the payment itself implies movement. The meaning of the terminal, and the biggest advantage of mobile terminals and other terminals is mobility. The two coincide, and the convergence of mobile payment and third-party payment has amplified this advantage.

Payment is the transfer of money from one account to another. The process of payment is the process of transferring money between accounts. In the era of electronic money, personal accounts must be indispensable for the currency to have both the attributes of payment and financial goods (if it is a cash transaction, it may not be needed). Payments are closely linked to the account. With the development of information technology, personal accounts will be gradually integrated. The future personal accounts will be a comprehensive account, integrating all personal business and all assets and liabilities. This account will become a personal financial activity or even daily life. Starting point and attribution point.

Second, the mode of mobile payment

According to the distance of mobile payment, we divide mobile payment into near-field payment, far-field payment, and online and offline O2O mobile payment mode. Far-field payment mainly includes online shopping payment, various payment, etc., while near-field payment is mainly used for transportation payment, supermarket shopping, and the like. The O2O mobile payment model is a mobile payment model between near-field payment and far-field payment, including far-field payment (such as online group purchase) and near-field payment (such as vending machine shopping). The main purpose is to achieve online and offline closed loop through payment, typically represented by scanning payment. In this paper, the classification of mobile payment types does not meet the standard of “no repetition and no omission†that should be strictly classified, mainly for the convenience of discussing problems.

In addition, according to the main body of mobile payment, it can be divided into bank-led mobile payment (such as M-Pesa, wing payment) and mobile payment led by third-party payment companies, such as Alipay's "touch brush" and WeChat payment. The focus here is on the mobile payment model classified by distance of mobile payment.

(1) Near-field mobile payment

Most of the near-field payments can be traded offline, without the need for networking. Typical representatives are NFC Mobile Payment (Google Wallet). If it is a near-field payment based on LBS technology, it needs a network to cooperate. The typical representative is Alipay's “Bumper Brushâ€. When both users “shake†the mobile phone at the same time, they can find the other party's account and make quick payment. Manually enter the other Alipay account. Of course, the "Bumper Brush" can also be "dropped" by NFC technology to find the other party. The premise is that both phones have NFC function.

Near-field mobile payment is mainly based on the following technologies: First, LBS technology refers to location-based services, which is a value-added service provided by a combination of mobile networks and satellite positioning systems (GPS). The location information of the mobile terminal user is obtained by using the cooperation of the mobile network and the mobile terminal. The second is NFC technology, referring to near field communication. The third is RFID, which refers to RFID technology, such as the RFID-UIM card for Wing Payment, which is a mobile phone card with wireless radio frequency function.

In addition, near-field payment also has technologies such as infrared and Bluetooth. However, the popularity of Bluetooth and infrared is not as good as that of NFC. This is because: First, Bluetooth and infrared payment cannot be paid when the mobile phone is out of power, and NFC payment can still be completed. Second, Bluetooth establishes a long connection time, infrared is more demanding for line of sight, and NFC payment is convenient and quick to establish a connection. Third, compared with RFID technology, NFC has the characteristics of close distance, high bandwidth, low energy consumption, etc. At the same time, NFC technology adds peer-to-peer communication function, the two devices of communication are peer-to-peer, and the two devices of RFID communication are master-slave relationship. .

In the process of mobile payment melee, NFC-based mobile payment has gradually shown certain advantages. The demand for mobile terminals based on NFC is too high, and its popularity is affected. In this regard, NFC-based mobile payment can be combined with LBS-based mobile payment to improve its popularity, such as Alipay's "touch brush".

(2) O2O mobile payment

O2O mobile payment is a payment made by connecting online and offline, and typically represents mobile payment based on LBS technology such as scanning payment. When you see the goods you like, scan the QR code and use the mobile phone to complete the payment, you can take the goods. This is the scanning payment, completely self-contained. QR code scanning payment can realize near-field payment (vending machine shopping, etc.), and can also realize far-field payment (group purchase, etc.). At present, QR code scanning is the main link between the connection line and the offline.

O2O mobile payment can also be completed by a mobile phone card reader, which is a mobile accessory (which can recognize different IC cards) connected to the mobile phone through the audio port of the mobile phone. This kind of terminal can not only realize far-field card swiping, but also complete near-field payment.

In addition, Facebook's Autofill mobile payment information automatic input function makes online and offline "interaction" more convenient. The operation principle is as follows: If the user purchases a credit card on Facebook, the user's credit card information will be recorded, and the user will automatically import their credit card information when using the Facebook account to make the shopping more convenient and quick.

(3) Far-field mobile payment

At present, most mobile payment performances are far-field payments, and typical representatives such as WeChat payment, mobile banking payment, SMS payment, voice payment, and Alipay payment. Payment is mainly achieved through mobile internet technology. Remote payment can be achieved by the following modes: one is the client mode, the other is the embedded plug-in payment mode, and the third is the mobile phone card reader mode.

Finally, it should be noted that the above three classification methods have no strict boundaries. Some payment methods can realize near-field payment, far-field payment, or O2O mobile payment. The close combination of the above three mobile payment modes can realize near field near payment, near field far payment, and far field far payment.

The main problem with mobile payment at present is that the standards are not uniform. For example, the three major operators in China have established their own mobile payment trusted service platform (TSM: Trusted Service Manager) to provide payment applications (such as finance and public transportation) in different industries; China UnionPay and some commercial banks have also built TSM, to cooperate with Operators provide financial payment applications. At the end of 2013, China’s mobile financial security and credible public service platform (“MTPSâ€) can solve this problem to a certain extent. At present, 7 institutions including China Construction Bank, China CITIC Bank, China Everbright Bank, China UnionPay, China Mobile, etc. Enterprise TSM has system level access trial operation. The completion of the mobile financial security and credible public service platform can realize the interconnection of commercial banks, mobile communication operators and third-party payment companies. The public service platform is a top-level architecture and is the standard of the mobile payment industry. Establish a healthy mobile financial environment with multiple corporate TSMs.

Third, mobile payment case analysis

(1) Analysis of typical cases abroad

1. Google Wallet. Google Wallet is mainly based on the NFC-based mobile payment model. It not only integrates the customer's credit card, but also integrates the customer's membership card, discount card and purchase card.

Google Wallet was mainly used for near-field payment. Due to the lack of popularity of NFC terminals (Apple's mobile phone does not support NFC), Google Wallet began to expand its use, not just for near-field payment. The physical card (physical card and Google Wallet account binding is introduced, and the payment is directly deducted from the balance of the Google account). The essence is the prepaid card, which can be used for withdrawals at the teller machine or for card consumption at the mall. In addition, Google Wallet also launched new features such as G-Mail mailbox payment, and cooperated with the instant purchase company to provide users and credit card information necessary for shopping, simplifying the process of users shopping online.

2. PayPal Beacon and Square card reader. At the beginning, PayPal launched mobile payment mainly for SMS payment, and then gradually transitioned to PayPalBeacon.PayPal Beacon is an accessory device that supports Bluetooth payment. With Bluetooth technology, you can complete payment without taking out your mobile phone (such as Bluetooth mobile phone call). . PayPal Beacon has two key points: First, Beacon does not need to access the Internet, and can be traded offline, which not only facilitates user payment, but also protects user data security to a certain extent. The second is to be able to realize the interaction between the merchant and the user in advance. When the user is close to the store that supports Beacon, the phone will vibrate or make a tone (of course, the user can also cancel this automatic reminder function). At the same time, Beacon does not continuously track the user's location to protect user privacy and data security.

The essence of the Square card reader is the card reader. By inserting the phone's headphone connector + application, you can complete the payment by credit card. Square also customized the bracket for the built-in card reader for the iPad, and the payment was made through the bracket. Square card readers are mainly mobile card payment, and Square's goal is to replace the physical credit card, and also provide a direct payment by Square account, in order to achieve true card-free payment, the principle is as follows: Square users install the Square application on the phone, You can checkout directly at some merchants.

3. Korea's MONETA and K-merce.MONETA are mobile payment brands launched by Korean mobile operator SKT, including MONETA card (using infrared technology, which can be traded offline), MONETA bill (online shopping), MONETA pass (passing card) ), MONETA bank (bank transfer, etc.), MONETA stocktrading (stock trading), MONETA sign (identity authentication), etc.

K-merce is a mobile payment service launched by Korean mobile operator KTF, similar to MONETA. Services such as mobile banking, mobile securities, and shopping payments can be provided. K-merce can be paid not only by infrared technology, but also by swiping the mobile phone.

4. Japan's Osaifu-Keitai.Osaifu-Keitai is a mobile wallet business launched by Japanese mobile operator NTT DoCoMo. The service is based on a contactless IC smart card called Felica. Users need to apply for a mobile wallet account in NTT DoCoMo in advance and pre-store a portion of the amount (a kind of prepaid payment).

The amount paid by the user to purchase the product using the service is directly deducted from the account, and the user is not required to enter a password (fast payment). In addition, Osaifu-Keitai can remotely lock and erase your data, while personal materials can be backed up to the cloud without worrying about losing.

(II) Analysis of typical domestic cases

1. Mobile phone card reader: La Cala and fast money. At present, there are two types of domestic mobile phone card readers. One is the Lakara mobile phone card reader, which is mainly for individual users (currently most mobile payment is also mainly for individual users). The advantage of Lakara is that it is paid by the convenience, and Lakara supports the payment of bankcards for all UnionPay logos. The business of Lakara mobile phone card readers mainly includes four major components, including banking services, life services, online shopping payments, entertainment and leisure. Specific services include transfer and remittance, water and electricity payment, recharge of credit, public donation, purchase of lottery movie tickets, Alipay recharge, etc. . The second is the fast money mobile phone card reader, mainly for corporate customers. Such as insurance companies, tourism, direct sales. Quickly brush similar to the foreign mobile payment product Square, insert the audio hole of the smart phone to establish a connection, you can use the credit card, bank card to complete the payment. A typical feature of the fast money mobile phone card reader is the no-card credit limit.

2. Telecom Wing Payment and Unicom's Worth Payment. Wing Payment is China Mobile's mobile payment product, which uses radio frequency technology to complete near-field payment. After China Telecom opens its wing payment account and stores the value, it can be used by China Telecom Alliance merchants and partner merchants. Wing payment can not only make far-field payment, but also make near-field payment. Far-field payment is done through websites, text messages, voices, etc. (far-field payment does not require a mobile phone), and near-field payment is done through a Wing Payment Card (RFID-UIM card).

Wopay is China Unicom's mobile payment product, using NFC function to complete near-field payment. Wo payment includes mobile client (mainly for far-end payment, such as group purchase), mobile wallet (mainly near-field payment, such as "brush" mobile phone shopping, ride), mobile phone card reader "War brush" (far field and near field) Payment can be).

3. WeChat payment. WeChat payment has an unparalleled advantage compared to other mobile payment modes due to its integration into the social network. Therefore, WeChat pays attention here.

(1) Development overview. Since the birth of WeChat payment in 2013, it has swept across China. At present, we support QQ recharge, Tencent recharge center, Guangdong Unicom, McDonald's and so on. The bank wealth management business is also cooperating with WeChat. Tenpay has already negotiated cooperation with a number of banks, and will try to focus on fixed-income products with less risk in the early stage. In addition, WeChat payment extends to the field of people's livelihood payment. For example, the “Shenzhen Power Supply†service officially launched by Shenzhen Power Supply Bureau can not only provide customers with business guidance, but also quickly inquire about various types of information such as electricity and electricity prices. And you can pay the electricity bill directly. Although small-scale people's livelihood payments are relatively thin compared to credit card repayments and e-commerce payments, this can increase user stickiness. In order to increase the convenience of payment, WeChat gradually cooperates with some merchants to promote voice payment, users can directly speak the goods they want to the mobile phone, and can directly pay. In addition, WeChat can also be purchased by scanning, that is, the user scans the QR code of the products in the store and directly pays for the purchase. In the process of WeChat payment, users do not need to quit WeChat and then enter other webpages or programs. As long as they have a bank card and a WeChat account bound to WeChat, they can purchase the goods provided by the public account through Tenpay. Less than 1 minute. However, the progress of financial institutions on WeChat payment is relatively slow compared to other industries. As of December 2013, more than 40 fund companies have opened WeChat accounts, but mainly for balance inquiry and business consulting. Most of them do not involve payment. If you need to purchase wealth management products, you still need to jump to the fund company's mobile phone page. The same is true for the banking industry. In addition, the on-line merchants of WeChat payment are basically merchants in mainland China. For the time being, they can only accept payment transactions from users in mainland China, and have not covered overseas regions. That is to say, WeChat cannot be used to purchase products across borders.

(2) Working principle. WeChat payment has two meanings: one is the fast payment through the third-party payment platform Tenpay, which is a kind of mobile innovation product; the other is the payment made by the WeChat public number opened by the bank to the mobile banking. We usually refer to WeChat payment in the first level of WeChat payment.

WeChat payment not only integrates the social network platform with third-party payment companies, but also integrates mobile banking to maximize the satisfaction of customers' payment needs. The operation process of WeChat payment in the first sense is as follows: WeChat users first need to add a bank card to their personal data to complete the binding with the bank card. When binding a bank card, you need to enter a bank card number, ID number, name, mobile phone number, and verify the identity by mobile phone number. If the above information is correct, the binding can be completed. In general, the user needs to set a WeChat payment password, and this password must be different from the bank payment password. Once the binding to the card is completed, payment can be made. Regarding the WeChat payment in the second sense, the bank first needs to open the WeChat public account. The WeChat users interact with the bank through WeChat, and guide the customer to the mobile banking through the WeChat platform to complete the payment, but only if the customer needs to open the mobile banking. . The core of WeChat payment is the integration of social network platform, third-party payment and mobile banking, making full use of the customer advantage of social network platform, the openness of third-party payment and the diversity of mobile banking functions. This is WeChat payment and other payment methods. The main difference.

(3) WeChat red envelope. WeChat red envelope is the product of the combination of WeChat and the traditional "red envelope". It is a new thing that is born by the spirit of the Internet and is an extension of WeChat function. As a social tool, WeChat closes the distance between people and is close to the real world interpersonal relationship and social attributes, which is the premise of WeChat red envelope activity and the result of WeChat red envelope activity. The WeChat red envelope is divided into two types: the spelling red envelope and the ordinary red envelope. The basic operations are as follows: fill in the red envelope information (amount, blessing, etc.) → WeChat payment → send a friend (group). Behind the process of sending and receiving red packets is the integration of Tenpay's recharge function, bank card withdrawal function and bank's payment settlement function.

A typical WeChat rush to red packets is as follows: First, establish a WeChat group (this is equivalent to "directional private placement"), and second, bind your bank card and charge the amount of red packets (such as 2000). The third is to send a red envelope at any time (you can also tell the group members the time to send the red envelope in advance). Once the red envelope is issued, members can compete in the group, and they can get the amount they have grabbed in the group, and compete with each other for "personality" and "luck" (because there are restrictions on the number of red packets and the total amount of red envelopes, and The amount of each red envelope is also randomly generated by the system).

According to data from Tencent, on New Year's Eve to 4 pm on New Year's Eve, more than 5 million users participated in the red envelope, and the total number of red envelopes received exceeded 20 million, with an average of more than 9,000 red packets per minute being received. The reason why the WeChat red envelope is sought after by users is as follows:

First, the hard-working red packets are actually red packets. The word "grab" means competition. Because of the introduction of the competition mechanism, it has increased popularity and increased the "yearly taste". Second, the WeChat "fat" red envelope conforms to the traditional Chinese Red packets are used to habits, and the "discovery" red packets are not in line with the Chinese people's habit of loving face. This is one of the reasons why Alipay's "new year's likable" is not as good as WeChat red packets. Third, the WeChat red envelope has got rid of the limitation of physical location. Although it is thousands of miles apart, it can also feel the joy of “the end of the worldâ€. Fourth, the WeChat red envelope reflects the spirit of the Internet, namely, sharing, equality, inclusiveness, democracy, etc. There is no distinction between high and low, not vanity, and some are only family, friendship and classmates. For example, elites and entrepreneurs from all walks of life have shown a childish side in the process of grabbing red envelopes.

Through the WeChat red envelope activity, the potential benefits of WeChat payment are as follows: First, the WeChat red envelope activity has enabled the WeChat payment function to be widely promoted. Most of the users who participated in the “Red Packet†have bound the WeChat account to the bank account. Second, some users who received the WeChat red envelope did not withdraw cash, making the red envelope become the deposit fund of Tencent. Tencent can benefit from depositing funds, mainly to eat interest. Third, the user did not withdraw cash after receiving the WeChat red envelope, which made the WeChat payment account become an account similar to “Alipay Balanceâ€, which forced Tencent to add more value-added services, such as recharging and selling financial products.

Fourth, the risk and supervision of mobile payment

The main risk faced by mobile payment is information technology risk, which refers to the risk of loss due to hardware defects, various software failures, network viruses, personnel errors, data transmission and processing deviations, and various network frauds. Behaves as a risk to customer accounts and funds.

Why is the risk of mobile payments mainly manifested in information technology risks? First, the mobile payment service mainly relies on an open network environment, and this open network environment is vulnerable to attacks. Second, security technology cannot keep up with the development of mobile payment. Different types of mobile payment service models are continuously introduced, and the technical support methods associated with them are not perfect, which may cause their payment business model to be at risk. Third, users pay too much attention to the convenience of payment and lack of awareness of risk prevention.

In short, the mobile payment method greatly reduces the transaction time and cost, and enhances the customer experience. However, the Internet is an open network system, which makes Internet finance have to face a more complex information environment than traditional finance, hacking and information theft. The potential risk factors of virus infection may lead to information technology risks to mobile payments and third-party payment. China has established a certain regulatory framework, including anti-money laundering laws, electronic signature laws and the "Opinions on Regulating the Management of Commercial Prepaid Cards". Regulations, as well as the People's Bank of China's "Measures for the Administration of Payment Services for Non-Financial Institutions", "Administrative Measures for Payment of Prepaid Cards by Payment Agencies", "Measures for Depository of Deposits for Customers of Payment Organizations" and "Administrative Measures for the Collection of Bank Cards" and other regulations The system can regulate mobile payment to a certain extent.

For mobile payment technology risks, in addition to the supervision of government regulatory agencies, mobile payment providers should also establish an overall risk control strategy (both technical and non-technical). Technical means such as: setting up a separate mobile payment password, SMS and voice authentication, using big data analysis to verify the identity of the person.

In addition, when information technology risks occur, it is necessary to promptly alert and make reasonable treatment of suspicious behaviors, providing real-time protection for user accounts. Non-technical means such as insurance provided by insurance companies, most mobile payment services provided by most third-party payment companies are currently insured.