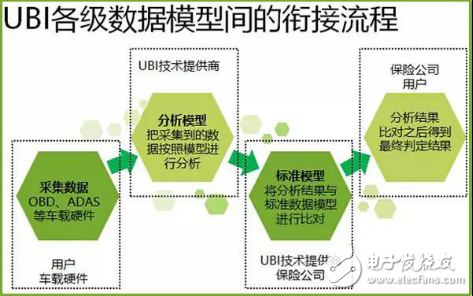

According to market data, among the 42 large property insurance companies with auto insurance business in China, 38 have losses in auto insurance business, of which 20 companies have losses of more than 100 million yuan, and 6 have more than 200 million yuan. The main reason for the loss is that domestic auto insurance is based on the pricing of new car purchases for a long time, which is very unreasonable. With the development of the commercial auto insurance rate marketization reform, UBI Auto Insurance (Usage Based Insurance) is considered to be an important weapon to improve the status quo of auto insurance business. In the European and American markets where insurance is already mature, traditional business growth is often only 2% to 3%, but UBI car insurance growth is as high as 20% to 30%. In the United States (US UBI auto insurance company Progressive Advance Insurance), Switzerland (MyMile), Italy, etc. Successful cases can be learned from many countries. In China, the concept of UBI auto insurance has always been a hot topic. From OBD, to ADAS, to car machines, rearview mirrors, car network practitioners are paying more and more attention to the combination of car networking and UBI. In the near future, UBI auto insurance has once again been pushed to the forefront as the China Insurance Regulatory Commission's commercial fare has changed again. The status of commercial vehicle reform since 2015 is as follows: On March 20, 2015, the China Insurance Regulatory Commission issued the "Opinions on Deepening the Reform of the Commercial Vehicle Insurance Clause Rate Management System." Since June 1, 2015, the six provinces and cities nationwide began to reform pilots (Heilongjiang, Shaanxi, Shandong, Chongqing, Qingdao). , Guangxi). From January 1, 2016, 18 regions will be reopened for commercial auto insurance marketization reform (including Tianjin, Jilin, Inner Mongolia, Henan, Anhui, Hubei, etc.). The purpose of the reform is to give the pricing power to the insurance company, hand over the choice to the consumer, and guide the insurance industry forward by market means through differentiated products and precise risk control. The favorable policies have brought new opportunities for UBI auto insurance to take root in China. At the same time, based on China's national conditions, it also faces many challenges. Figure: UBI car insurance is an insurance pricing technology based on vehicle usage and driving habits Component factors in the UBI data model The key and difficult point of doing UBI auto insurance is not only to collect real-time data on vehicle driving conditions, but also to establish scientific data models and algorithms, estimate the driver's risk coefficient from complicated data, and then provide pricing basis for premiums. . The improvement of the UBI data model requires the complete construction of a two-part data model. First of all, it is necessary to collect a lot of data such as the user's mileage and driving behavior through the device, and also combine certain risk data, and then divide the data according to different weights, and obtain the driving behavior score through preliminary calculation, that is, construct A preliminary analysis of the data model; in addition, based on the actual situation of the insurance company (such as the income and expenditure ratio of insurance companies, etc.) to build a standard data model. The former is compared with the latter, and the final analysis result is obtained as the basis for premium pricing. So, what should be included in the collected data? At present, most of the most common UBI auto insurance models on the market are built based on driving mileage. The single factor of risk assessment can not truly depict the important “human factor†characteristics of the driver's behavior insurance pricing; A variety of factors, the promotion of risk management and control is relatively limited, and is not conducive to the introduction of personalized insurance products. The author learned from 芮锶钶 (Shanghai) Network Technology Co., Ltd. that the company is evaluating each journey of the user with a calculation method that sets more risk factors, and calculates each trip after the end of each journey. The corresponding score, which is multiplied by a different weight ratio, yields the final cumulative score. This allows for more flexibility in matching the data model, with higher accuracy and more complex calculations. The data model of 芮锶钶 is based on the UBI model verified by millions of car owners abroad, fully localized and personalized. In the whole data model, driving behavior, driving environment, form distance... These data are subdivided into multiple sub-data factors, which can be classified into “user portraits†according to the classification of main factors, secondary factors and cofactors. The main factors generally include speed, urban road, night time, rapid acceleration, and sudden braking. These five main data are combined with the secondary factors such as the single travel time and distance of the vehicle and the speed limit of the surrounding roads. Driving behavior. In addition, there is a special analysis in the UBI data model, which is the evaluation of risk data. Driving risk assessment requires the collection of driver attributes (age, driving age, etc.) and behavior, vehicle conditions, road conditions, environmental factors, management factors, etc. These data also calculate risk data based on different risk weight ratios. The construction of UBI upstream and downstream industry chain ecology Auto insurance is a hard demand, and the market potential is huge. UBI, which can meet the insurance pain points, meet the needs of car owners, and adapt to the development of mobile Internet, will become a new development direction and solution for China's insurance industry. This new solution requires a full industry chain to build. Although there are many companies claiming to be engaged in UBI in China, there are not many companies that are really advancing from the bottom of technology and the ecological level. For example, the company is currently engaged in the construction and research and development of the UBI data model, and has extensive cooperation with insurance companies, OEMs, TSPs, and automotive after-service providers. As the core technology of UBI data model, we are striving to build an open platform with safe driving as the core. In the process of connecting with different enterprises, the services and support are not the same. For example, last year's claims The rate is much higher than the insurance income, the insurance company needs to control the claims expense, which requires a good algorithm to determine the profit of the big insurance company after discount, the small insurance company prefers to get more customers through the UBI system. . In terms of cooperation with the OEM, 芮锶钶 provides quality insurance and services to car owners by pre-installing software on the car to get through the driving habits and insurance pricing and claims-related channels; in addition to the OEM, and the automotive aftermarket smart car hardware For example, OBD, interior mirrors, driving recorders, etc., and even mobile phones can cooperate. The driving behavior data can be collected by opening the SDK interface or pre-installing the APP. to sum up Although the momentum is hot, UBI's promotion and landing in China will take some time, mainly because: First, the UBI insurance model has a wide industrial chain, including data acquisition end (may be software, hardware, and may be the main engine factory, before Installed), data models (ie, analytical models and simulation models), insurance companies (product providers), service providers (TSP, 4S stores, etc.), users (data providers, product buyers), etc., need to work together. Secondly, there is a certain error in the data collected by GPS and G-sensor at present. Therefore, in the process of final landing of UBI insurance, certain algorithm optimization is needed, or through cooperation with the pre-installed OEM. The accurate collection of data can achieve the ultimate UBI insurance model, which is the direction that the team or enterprise that is currently engaged in the development of the UBI project needs to be deeply rooted. Third, the flexibility of the policy is the source of industrial development momentum. The China Insurance Regulatory Commission needs to formulate new laws and regulations as soon as possible to accelerate the completion of UBI. Fourth, there is only an insurance company that pays for UBI. The driving force is not obvious, and more business models and plans are needed to drive development. However, we have also seen pioneers like 芮锶钶, and major insurance companies are planning the layout intensively, which is a good start for the unchanging yesterday. MR11 4w DIM led Spot Light is lighting with the size of the cup.

MR11 4w DIM Led Spot Light Cup points not connected with 12V and 220V transformer transformer, such as you are, then spotlights with transformer.

What you need is 12V 35W MR11 halogen lamp cup.

Lampholder two pins at different distances, MR11 4w DIM led Spot Light feet away from the common general 4mm; MR16 lamp pin pitch is generally 5.3. Some lamp base jacks are oval, light bulbs foot distance 4,5.3,6.35 apply; some lampholder socket is circular, applies only to one kind of bulb from the feet.

Low-voltage MR11 4w DIM led Spot Light constant current drive, wall lights, spot lights, buried lights, underwater lights, automotive lighting

Mingxue Optoelectronics Co.,Ltd. has apply the I S O 9 0 0 1: 2 0 0 8 international quality management system certificate, For MR11 4w DIM led Spot Light, we apply the CE, RoHS and SAA certificate for our led lighting product.

MR11 4w DIM led Spot Light Mr11 4W Dim Spot Light,Cob Mr11 4W Dim Spot Light,Bedroom Mr11 4W Dim Spot Light,Kitchen Mr11 4W Dim Spot Light Shenzhen Mingxue Optoelectronics CO.,Ltd , https://www.led-lamp-china.com

Spotlights lights Cup MR16 and MR11 are divided into two, the former is the headlight cup, which is a small lamp cup

â—† industrial low-voltage lighting drivers

â—† Low voltage industrial lighting

â—† LED back-lighting

â—† Backlight LED Driver

â—† emergency lighting system

â—† LED driver

â—† a variety of low-voltage equipment need constant current drive