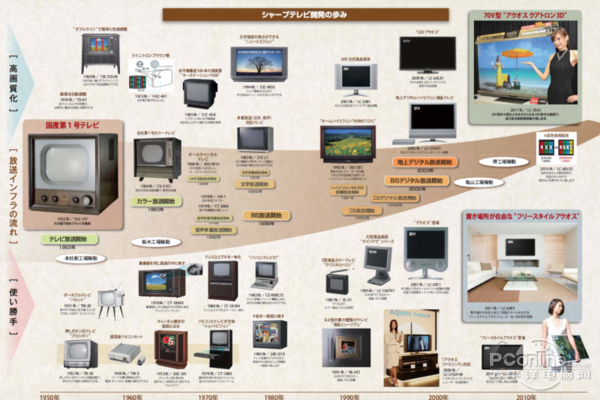

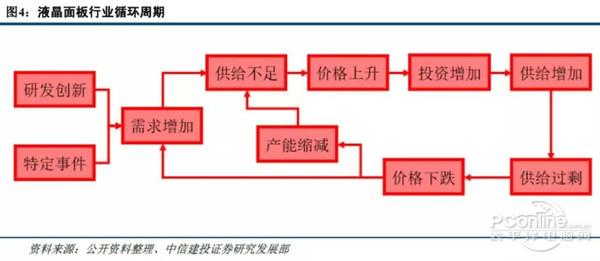

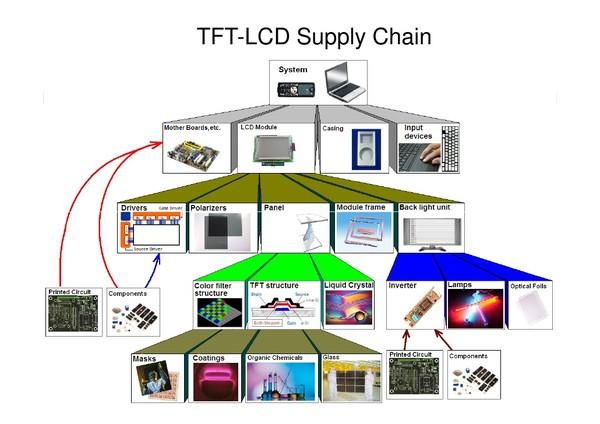

[PConline News] When it comes to the LCD industry, most of the well-known LCD companies are Samsung Display (LG Display), Domestic (BOE, Tianma), and Taiwan (AUO, Chi Mei). But the Americans who invented liquid crystal technology are the Americans, and it is the Japanese who have made extensive use of liquid crystal technology and technological breakthroughs. The "hegemony" of the LCD industry has been changed from the United States, Japan, and South Korea to China four times in less than 60 years. Next we analyze the situation of the LCD industry from the perspective of "liquid crystal cycle". Before the birth of LCD technology, CRT display technology was already available. When the American Radio Corporation developed the first LCD display model, they were both excited and disappointed. The excitement was the birth of a brand new display technology. Disappointed that this display technology did not seem to be as mature as the CRT technology. Monotonous, correspondingly slow, small size, there is no way to use flat-panel TVs. However, the Japanese who saw this technology had a keen interest in it, and first used it in the watch industry, and later in the fields of calculators, instrument displays, etc., and eventually applied to flat-panel televisions. In the cycle of continuous R&D, production, product application and technological breakthrough, Japan has almost crazy input in LCD. By the 1990s, Japanese companies almost monopolized the entire LCD market. Companies represented by Sharp as the “LCD craftsman†spirit have made tremendous contributions to the development of LCD technology. However, after a long period of time, when LCD production entered the first cycle, Japan's LCD industry began to face one crisis after another. The LCD screen is divided by generations, which refers to the ability to cut the size of the LCD panel. Higher-generation production lines can produce panels with larger dimensions. In the era when the demand for liquid crystals continues to increase with size (approximately 1.8 times every three years), the high-generation production line represents a broader competitive advantage. For example, LCD monitors that can only be used for watch sizes can be produced at first. In order to use LCD panels in notebook displays, flat-panel TVs, and other products, it is necessary to build higher-generation liquid crystal production lines. The LCD industry has created a unique “liquid crystal cycle†based on the characteristics of the generational division. For example, when the 10.4-inch notebook display satisfies the market demand, panel companies will flock and begin to invest in the production of LCD panels of this size, and soon the supply exceeds demand, and each company's profits plummet or even fall into losses. However, the high price/performance ratio brought about by the drop in panel prices has enabled the rapid expansion of the application of liquid crystal displays, which has led to an increase in the price of under-capacity products. Companies have again invested in expanding production. This cycle is the "liquid crystal cycle." Once the “release of production capacity†and “expansion of demand†cannot be accurately linked, it will cause sharp fluctuations in the profitability of the LCD industry chain. The LCD industry is different from consumer products. It is an industry that gradually “creates†demand because LCD panels have more and more extensive application scenarios. Japanese companies did not understand this rule. When the "liquid crystal cycle" entered a recession in 1993-1994, it faced losses, cut production, and cut staff. At this time, Korean companies recruited Japanese engineers who had been "retired" to start frantically investing in higher-generation LCD panels. When demand for larger panels was created, Japanese companies obviously could not keep up. In 2001, it was through the 5th generation LCD production line that the Samsung and LG companies completely surpassed Sharp and other Japanese companies. The defeat of Japanese companies was not just a result of the “liquid crystal cycle†failure, but also the deep-rooted obsession with “unique skills†of Japanese companies, which made it impossible to adapt to rapidly changing market demands and missed the market step by step. Japanese CRT and plasma technology in the era of vacuum tubes, through "unique stunts", such as "single shot three bundles", "Tili", "diamond enamel" and so on, have indeed gained a very high reputation, and also brought great products Sales. However, as a liquid crystal display technology for semiconductor technology, it has moved toward modular and standardized production. There is no fundamental difference between the product technology and quality of each product. The entire industry’s competitive approach is no longer a technical-theoretic hero, but instead becomes a competition between R&D speed, supply chain management, cost control, and marketing promotion. The biggest innovation in the modern electronics industry is essentially the improvement in efficiency brought about by the separation of hardware and software. For example, Apple will focus on product design and R&D, and OEM production will be handed over to a foundry like Foxconn. However, Japanese companies are initially rejecting this innovative model. They are persistently convinced of designing and manufacturing vertically integrated business models, and they also want to use this approach to create differentiated, unique skills. However, the Japanese did not expect that the changes in the electronics manufacturing industry would be so rapid and that the vertical integration model would be too late for innovation to be shot on the beach by more efficient companies. Look at the current mobile phone is basically a half-year update, the cycle time of design and development is already very tight, if you want to own production, once the design update, product iteration, the entire product line must be reorganized, not only the high cost of innovation, The cycle of innovation will certainly be lengthened. What are the competitive advantages? If you only need to consider the upgrading of product design, production and manufacturing will be handed over to a representative factory like Foxconn, that companies will be lightly loaded, there are more opportunities to enhance product innovation. It is in such a highly-commercialized commercial society that China has risen to the top. Chinese LCD panel makers have also won tremendous opportunities in the surging LCD industry through their overall acquisition of Japanese and South Korean companies, their ever-accumulating factory technology, and their frenzied investment in counter-liquid crystal cycles. How important is tight division and collaboration and supply chain networks? A large number of small and medium-sized enterprises have gathered on the southeast coast of China, and the specialized division of labor of each company has reached a very fine level. For example, in the appearance of the product mold companies, divided into design, machining, finishing processing. In terms of design, it is divided into CAD and CAM; in the machining direction, it also distributes electrical machining, wire cutting, and NC machining respectively; and in the finishing process, it is divided into detailed divisions such as grinding and assembly. Once there are new innovation needs, thousands of supply chain networks can be quickly reorganized and efficiently cooperated with production. This kind of network with scale, efficiency, and flexibility is not available worldwide. Many people feel that the LCD industry cannot play at all because there is no technology. What can the Japanese know about technology? In fact, the LCD industry is not only required to have patented technology developed by the laboratory, but also a large number of factory technologies that have been groped out. Although the technology of the factory is not so inscrutable, it requires a lot of details to improve and tips to accumulate, and eventually it will become a powerful technology difficult for competitors to copy and surpass. Against this backdrop, Chinese LCD companies have made intensive progress. Like BOE, the largest panel maker in China, its current shipment volume has accounted for 22.3% of the world's total, surpassing South Korea’s LGD, and it has won the world’s No. 1 throne. LCD companies in mainland China, Taiwan, and Japan and South Korea have not had much difference in the quality of LCD panels. Prices are also on the same level. Many Japanese and Korean TV brands use domestic LCD panels. Of course, the rapid development of the domestic LCD industry in recent years is inseparable from the government's investment. The development of new liquid crystal production lines is always tens of billions of investments, and the profit cycle is relatively long. Few capitals are so generous when they do not see short-term benefits. Only by investing in the government's shares can the capital be successfully financed. In addition to capital and technology, it also requires the support of local government policies. The employment of people, electricity, land, roads, water and sewage must all be supported by the government. The LCD industry can develop in an orderly manner. Shockproof Armor Phone Case For IPhone Shockproof Armor Phone Case For Iphone,Shockproof Armor Phone Case,Shockproof Armor Iphone Case,Best Shockproof Armor Phone Case Guangzhou Jiaqi International Trade Co., Ltd , https://www.make-case.com

Summary: The LCD industry has changed hands and is also a symbol of the change in the pattern of the electronics industry in China, Japan and Korea in recent years. The impact of the liquid crystal cycle on investment strategies, the impact of the global industrial chain division and collaboration on industrial innovation, and the impact of policy conditions on industry survival and expansion , are slowly changing the game of the LCD industry, the survival of the fittest is the most important.